Three-Fund Portfolio Rebalancing Calculator

Your Three-Fund Portfolio doesn't stay balanced on its own. The market moves, allocations drift, and that 65/25/10 split you chose quietly becomes 72/20/8 while you're busy working.

This calculator fixes that in about 30 seconds. Enter your current VTI, VXUS, and BND balances, set your target percentages, and it tells you exactly what to buy and sell. Done.

You can also add extra funds as you rebalance.

New to rebalancing? Read the full guide to rebalancing your Three-Fund Portfolio for the why, when, and how. Got more than three funds? Use the Large Portfolio Rebalancing Calculator instead.

Three-Fund Rebalancing Calculator

Enter your target allocation and current ETF balances. We'll tell you exactly what to buy or sell to get back on target. Twenty minutes, once a year.

What mix did you choose? Pick a preset or enter your own.

Log into your brokerage and enter the current dollar value of each ETF holding.

| Fund | Current Balance |

|---|---|

| U.S. Stocks VTI / SCHB |

$

|

| Int'l Stocks VXUS / SCHF |

$

|

| Bonds BND / SCHZ |

$

|

Entering new money here lets the calculator direct it toward underweight funds first — so you buy less and sell less. Works great for taxable accounts.

Your Rebalancing Results

| Fund | Current Balance | Target Balance | Difference |

|---|

Here's exactly what to buy or sell to get back to your target allocation.

💡 Inside a Solo 401(k) or Roth IRA, selling to rebalance has zero tax consequences — buy and sell away. In a taxable brokerage account, try directing new contributions toward the underweight fund to avoid triggering capital gains tax. Don't stress if you're off by a point or two — close enough is good enough.

Frequently Asked Questions

How often should I rebalance my Three-Fund Portfolio?

Once or twice a year is plenty. I do it quarterly when I make my Solo 401(k) contributions — it takes about five minutes. If any position has drifted more than 5 percentage points from its target, rebalance. If not, leave it alone.

Does rebalancing inside a Solo 401(k) or Roth IRA trigger taxes?

No. Buy, sell, trade all you want inside tax-advantaged accounts — no capital gains taxes. That's one of the big advantages of investing through a Solo 401(k) or Roth IRA. In a taxable account, rebalancing by directing new contributions into underweight positions avoids selling and triggering taxes.

What if I have more than three funds?

Use the Large Portfolio Rebalancing Calculator. It handles any number of positions — four funds, six funds, whatever you've got.

Vanguard founder Jack Bogle:

“Don’t look for the needle in the haystack. Just buy the haystack.”

Two IRS rules let you access retirement money before 59½ without the 10% penalty. Here's how Rule 72(t) and the Rule of 55 actually work for freelancers.

Freelancers get access to some of the best tax-advantaged accounts in the tax code. Here's the full list — what each one does, how it's taxed, and which ones to open first.

Your sub-5% mortgage costs you less than your portfolio earns. That gap is free money — make extra mortgage payments, or invest. Let's run the numbers on $200 and $500 a month.

That 1% annual advisor fee doesn't sound like much. But on a $630,000 portfolio over 17 years, it quietly drains nearly $480,000 from your retirement — while the same money in a low-cost index fund does none of that. Here's what the financial industry would prefer you never actually calculate.

Someone in the Trump administration is leaking market-moving information. Your portfolio is the loser.

Form 5500-EZ exists to prove your Solo 401(k) is still alive and in compliance. File it late, and the penalty can decimate your retirement savings. Here's everything you need to know.

The income tax system works like a layer cake, not a cliff. Understand the 2026 federal tax brackets, how your freelance income flows to taxable income, and how Solo 401(k) and HSA contributions slice off the most expensive layers.

Freelancers can shelter up to $96,250 in 2026 using three tax-advantaged accounts. Learn which to open first and how much you can contribute.

Rebalancing is simply bringing your portfolio back to your target allocation. That’s it. No spreadsheet pain. No Wall Street jargon. Better yet, I have a nifty calculator to do the math.

Here we go, 2026! What could possibly go wrong, right?

Read about the new 2026 limits for the i401(k), also known as a Solo 401(k). Plus the Roth and Backdoor Roth IRA, and the awesome HSA.

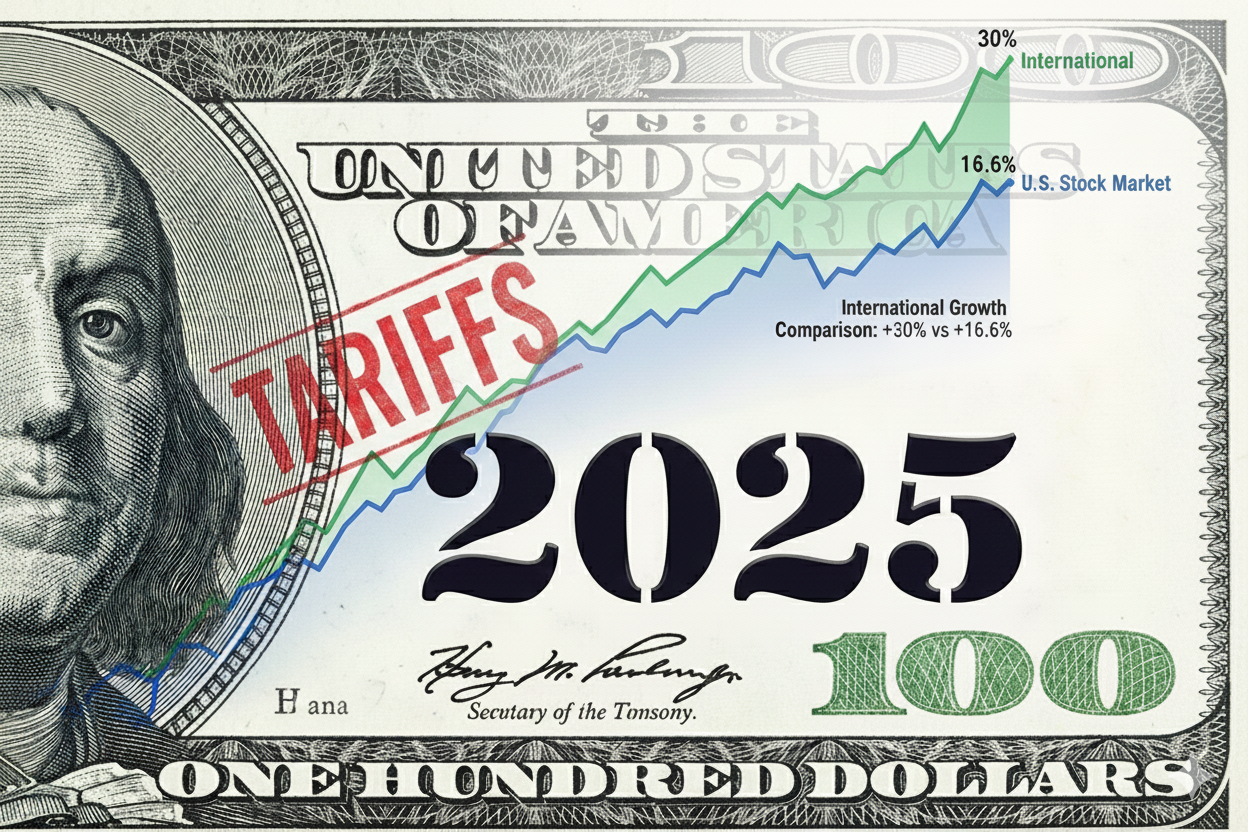

How did 2025 turn out? - The U.S. market coped with some novel pressures and the vibecession continued. Meanwhile, International outperformed.

Did you have a terrible year financially? That painful low-income year might at least have a silver lining. If you had a bad year, your marginal tax rate will be lower than usual, so now might be a good time for a Roth conversion.

Max out the contributions to your retirement accounts before year's end. Now is the time to get your QuickBooks in order and talk to your accountant before the end of the year. Don’t wait.

The freelancer investment trinity — i401(k), HSA, and Backdoor Roth IRA.

The Robinhood Gold Card is a great deal for investors; instead of trying to use points to shop or travel, we’ll invest the unlimited 3% cash back and spend big later in life.

Are you freelance or self-employed in your 40s or 50s without retirement savings? You're not screwed. Here's the math: Start investing $2K/month at 50, and you'll have $600K by 65. The biggest mistake isn't starting late—it's not starting today.

Freelancers, let's talk about the elephant in your home office: retirement savings.

The ‘Retirement in the USA: The Outlook of the Workforce - 2025’, survey from the Transamerica Center for Retirement Studies is out, and it’s an eye-opener.

While your traditionally employed friends have HR departments force-feeding them 401(k) plans, you're busy trying to figure out if you can expense that second monitor as a business expense.

How much emergency fund do freelancers and self-employed individuals need? Compare HYSA, Treasury ETFs like VBIL, and other options for self-employed workers. State tax savings tips included

The Roth IRA — With simple set-and-forget investing, it’s easy to have around $1 million in retirement.

It’s often misunderstood how the states and feds tax us. A misconception is that once someone hits a certain income, all of their hard-earned money gets taxed at a higher rate. This is not the case.

2024 — The markets, a Trump election victory, and whatever happened in your freelance industry. What did it all mean for our i401k portfolio and the goal of chill-retirement?

Forget the outdated retirement stereotype of working until you drop, then shuffling off with a gold watch. As a solopreneur or freelancer, you can design something better: working less while your investments pick up the slack. The question is: how big does that investment portfolio need to be?

The Three-Fund Portfolio — Freelancers, it’s pretty much the only investment we need in the stock market. U.S. Stocks, International Stocks, plus Bonds

More in our series of ‘More for us, less for you IRS!’

Below is a list of the various tax-advantaged accounts we can have as freelancers. Learn the ways of the force, I mean accounts. As freelancers, investing is our ultimate side hustle.

The stock market is often widely misunderstood due to the hype in the media reporting on short-term market moves. That and the jibba-jabba of your next door neighbor or some guy in a bar. It’s the long term that matters. We need to ignore the noise.

The Beneficiary Ownership Information Report.

UPDATE: As of March 26th, 2025 the whole thing got thrown out. Now only foreign companies have to fill it out.

Vanguard exits managing i401k accounts - but we still love their ETFs and funds. Let’s chat about what i401k provider to use.

The HSA (Health Savings Account. Make your out-of-pocket medical expenses a sweet tax deduction. The money is always yours; it’s not ‘use it or lose it.’

The Mega Backdoor Roth is a strategy for freelancers with a Solo 401(k) to contribute beyond the normal employee and employer limits, using after-tax contributions that get converted to Roth