Is your Solo 401(k) balance over $250k? — File Form 5500-EZ, or be fined up to $150,000.

The 'don't blame me' blurb: I am not a financial advisor, portfolio manager, or accountant. This is not tax or investment advice; it's information to get you going. Please consult your trusty professional and do your due diligence. Carry on!

The dumpster fire you will cause if you don’t file this form

TL;DR

You must file Form 5500-EZ if your Solo 401(k) balance goes over $250,000 at any time during the year. Yes, even if it later drops back below $250k.

Fines of $250/day, with a maximum of $150,000 per year, await if you don’t. (Yes, it’s truly f***ing absurd they could be this high.)

If you are just finding out about this, you must file all past years where the account was over $250k. There is a penalty relief program with a max. total fine of $1,500. Here is the IRS forgiveness program for that little gem.

The form is due on July 31st for the previous year. 2025 is due on July 31st, 2026.

Your accountant may not warn you about this. Mine at the time didn’t, and Schwab doesn’t either. Some Solo 401(k) providers will contact you and give you a nudge.

Also known as an Individual 401(k), Self-Employed 401(k) and One-Participant 401(k).

Form 5500-EZ — What’s the deal here?

With fines that massive, you’d think it’s a matter of national security. Nope. The form only asks for basic plan details, the number of participants, and the starting and ending balances of your Solo 401(k). The fines are idiotic and completely out of whack with any harm you could be doing if, somehow, you were messing up your Solo 401(k).

The form is a Department of Labor/IRS collab. Don’t ask, just fill it out while your clients all lose their minds because you’re not paying attention to them.

The first time you file, it’s a pain in the ass to get all of the details. Then, every year after, you just use the same details and update the amounts in your Solo 401(k).

Just don’t forget to do it. Save the form each year in a folder on your computer, so you can refer to it the next year. I’ll remind you each year on the website or on social media. You’re welcome.

How to file it by mail

You can file it by filing out the form here, but only if you're NOT required to file at least 10 returns of any type with the IRS during the year. S-Corp owners, it may be safer to file online as we have multiple forms, 1099s, etc. to file throughout the year.

IRS page to download the form, print, and mail.

Send to:

Department of the Treasury Internal Revenue Service

Ogden

UT84201-0020

Filing online

To file it online, you use the EFAST2 portal here. Create an account if you don’t have one. You will receive a user ID and a PIN.

Here we go:

Below is how to fill out the form. The obvious parts I skip over, like your address, horoscope sign, etc

Download the December 31 account statements from your provider (mine is Schwab) for your Solo 401(k). If you have both a pre-tax Solo 401(k) and a Roth Solo 401(k) account, add the totals together. They have to be with the same provider, and will be sub-accounts under the same plan. It’s a problem if you have two Solo 401(k)’s with different providers; it’s not allowed.

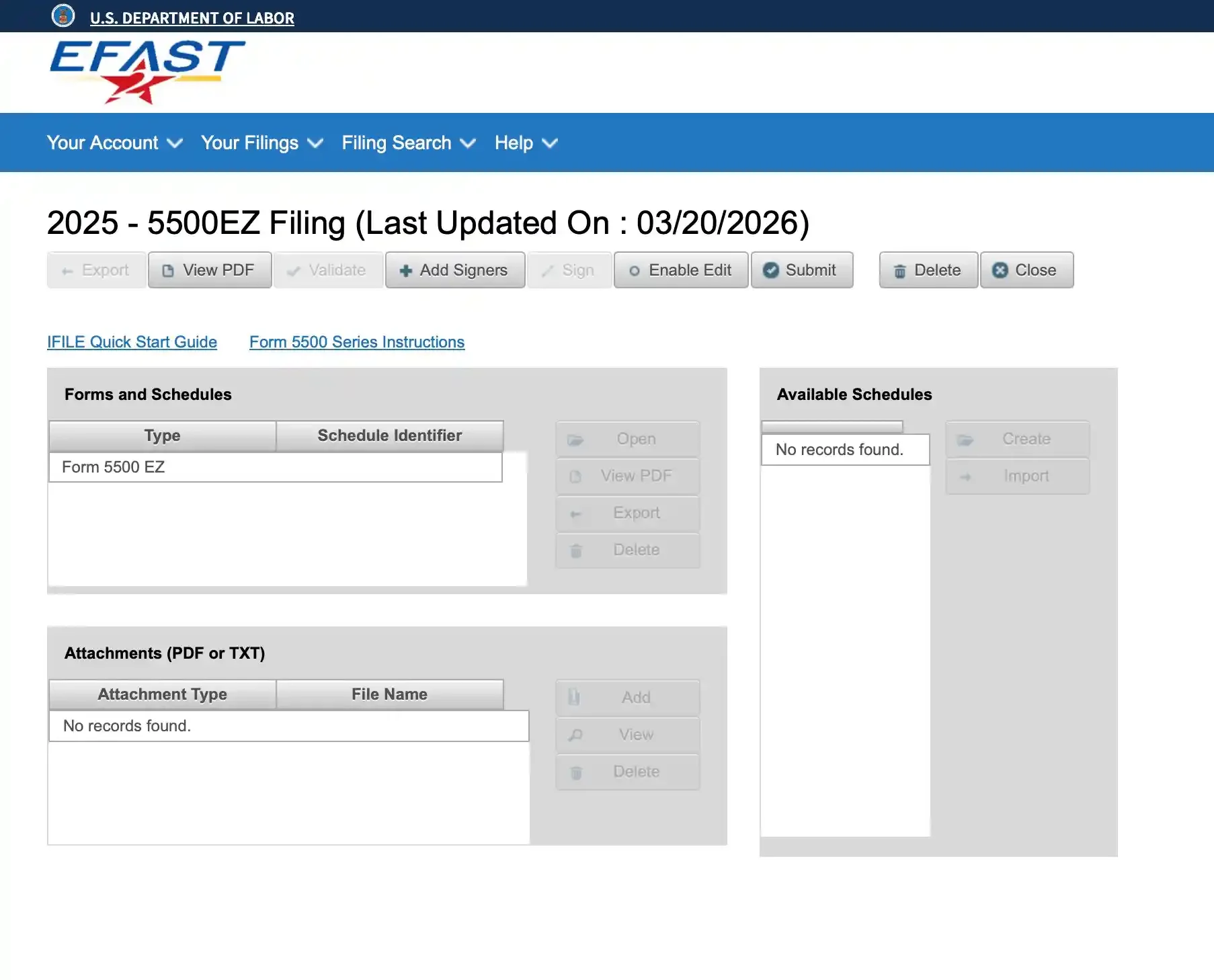

Login to EFAST2. (This is a Department of Labor site, not the IRS. Log in with a Login.gov user and password. If you don’t have one, you can create an account.)

Click ‘Create a Filing’, on the next page

Create a filing

I know, I know

Click ‘I know which Form 5500 Series I want to complete.’

Select Form Year and select: 2025 - 5500-EZ or, the year you want.

Name it anything you like.

Hit ‘Create.’

Part I

I did not need to check any boxes; it’s not required (confusing, I know). I just used the calendar dates for the report you are filing.

If it’s your first 5500-EZ, Check A

If you need an extension for some reason, that is Box 5558

Check D for the penalty relief program.

Part II

The good news after the first time you file this, you can just copy and paste all of this info from the prior year’s form. The first time its a PITA.

1a - Enter the name of the plan. You would have named your plan when originally filling out the Solo 401(k) application with Schwab, E*trade, etc. If you can’t remember, call your provider and ask them.

1b - Enter the plan number. It will also be on your Solo 401(k) application form when you open the account as above. It’s a number you had to specify, and it's likely 001.

2a Employer’s name is your company name

In care of name is your name

2d Business Code. Click the Blue link and select a code that matches your biz as best as possible.

3a Plan Administrator’s Name - That’s you. You’re the plan admin, so write ‘Same’.

3b Administrators EIN - That’s your compani’s EIN. (Even if you’re a sole trader, you have an EIN. You had to get one to open the Solo 401(k).

Part III

6a Total Plan Assets Look at your Solo 401(k) December statements to get this info. It’s the end of the statement balance for December 31st.

Beginning. If you filed out a 5500-EZ in the past year, the beginning of the year is the prior year's end-of-year total. If this is your first time in 2025, check your Dec 2024 statement to get the beginning-of-year figure. That is the beginning of 2025 number.

If you took a loan from your plan, it would be included here by default, as the loan would have reduced the assets. Do not put the loan in 6b below.

End Look at your Dec 2025 statement. If you have a pre-tax and a Roth Solo 401(k), add the totals. (Yes, you can have both a Pre-tax and a Roth, but the limits are shared, and they must be on the same plan with the same provider.). Check the Solo 401(k) guide here for a refresher.

6b Line 6b (liabilities) would only be relevant in unusual situations where the plan itself owes money to someone, like an unpaid expense or, in more complex plans, acquisition indebtedness from leveraged real estate inside the plan. That essentially never happens in a plain-vanilla Solo 401(k).

7 These are the contributions that you and your company made to your Solo 401(k).

— Remember, as an employee, you get a set contribution limit, then your company can add 20% of the “net earnings from self-employment” for Sole Traders, or for S-Corps, and an additional 25% of the W-2 amount that you paid yourself.7a Employers (Your company’s contribution to your Solo 401(k))

7b Participants (Your individual contribution)

7C N/A

Part IV

Plan Characteristic Codes: Click ‘ Add New Code’ and enter each number. Yes, this is confusing.

Originally, I called Schwab to ask them for the codes. The rep. said they could not provide them as it was deemed ‘tax advice.’ Interesting. They created the plan; they should know what they are. There is a blue link that shows the codes on the page; they are also at the end of the PDF instructions (link at the bottom of the page)

Select Defined Contribution Plan. (This means it’s a plan where we decide the contributions that go in. We don’t have a defined benefit amount that is set to pay out later.)

The codes I used (Yours are probably the same, but check the descriptions):

2E - Profit Sharing Plan (That is the employer match — your company’s match, part)

2J - Section 401(k) feature. This is our ability as an employee to add funds to the Solo 401k).

3B - Plan covering self-employed individuals (Obviously!)

3D - Pre-Approved pension plan — If you got your plan from Schwab, ETrade, etc., or Mysolo401k, then the plan is pre-approved.

Part V

9 Did you take a loan?

10 No. We don’t have a defined benefit plan (that means you get an agreed payment in retirement, forever, like the old school pensions that employees got)

11 Minimum finding requirements question is NO

12 ‘Opinion Letter date and Opinion Letter Serial Number.’

The first time I had to fill out the 5500-EZ I called Schwab, and they guided me to it. It’s a letter from the Department of the Treasury to Schwab on page 35 of the Schwab Basic Plan Document here. You may have to call your provider to get it.

The Home Stretch

Now click ‘View PDF’ link at the top of Part V and save it. Use the details for next year.

Click Save and Close. BUT, you are not done yet.

This takes you to this screen that is very, ‘we are the government, so you figure out the bureacracy here’.

Click Validate, and it will scan the form for missing fields or obvious problems. If anything comes back flagged, fix it and re-validate. If it comes back clean, you're good to proceed.

Then, Click Sign to begin the 3-step process.

Step 1/3 (Validate Filing), a pop-up window displays the Plan Name, Sponsor Name, Plan Number, EIN, and Plan Year dates. If no errors are found, you'll see a message that the filing is ready to sign. Review those details carefully — make sure the EIN and plan number are correct before proceeding.

Step 2/2 click Accept Agreement

Step 3/3 You'll need your EFAST User ID and PIN — these are separate from your Login.gov password. You can view your User ID and PIN from the Filing Summary page after logging in.

I selected Plan Administrator and Employer as the signer.

Click: Sign. You then get a ‘Sign Confirmation Page’

Click Go to Filing Menu

You will now see that Validate and Sign are grayed out.

Click Submit. You will get a submission confirmation. Click Print this page, save it as a PDF and keep it! The system also sent me confirmation emails, keep them too.

The end!

Grab a beverage, you deserve it

Yes, the glory and freedom of being your own boss. If you’re like me, by next year, you will have forgotten how to do a lot of this. The good news? You can use 90% of what was on last year’s form, and also come back here if you can’t remember how to navigate the last bit.

Just remember to file this form, as the fines are potentially huge. The minimum is $500 under the forgiveness plan, but if that doesn’t work, it’s up to $250/day, capped at $150,000 per year.

The form is due July 31st. Don’t screw this one up, if you do, they are coming for you.

Do you really want the IRS eyeballing you over a form?

The Mega Backdoor Roth is a strategy for freelancers with a Solo 401(k) to contribute beyond the normal employee and employer limits, using after-tax contributions that get converted to Roth