The Hack to Max Out Your Solo 401(k) — The Mega Backdoor Roth

The ‘don’t blame me’ blurb: I am not a financial advisor, portfolio manager, or accountant. This is not tax or investment advice; it’s information to get you going. Please consult your trusty professional and do your due diligence. Carry-on!

Your accountant might not know about this backdoor.

TL;DR

The Mega Backdoor Roth is a strategy for high-income earners to hit the yearly maximum allowed contribution for a Solo 401(k). In 2026, the maximum limit is:

Up to age 49 = $72k

Age 50+ = $80k

Age 60-63 = $83.25k

Why do it? To take advantage of the tax-free benefits of a Solo Roth 401(k) account instead of using a taxable brokerage account, and later paying capital gains tax.

A specialized Solo 401(k) plan is required through providers such as MySolo401k or Nabers Group. That plan then works with a brokerage like Schwab or Fidelity.

This is NOT a Backdoor Roth IRA. That’s a completely separate account and set of limits. You can have both every year. How sweet is that?

Staffers, this works for you too if your employer’s 401(k) plan allows after-tax contributions.

I don’t receive referral fees from any of the companies mentioned in this article. It’s unbiased education only.

The Mega Backdoor Roth

Another in the series of, ‘WTF! My accountant never mentioned this.’

You have maxed out your Solo 401(k) with your individual and employer contributions. You've done the regular Backdoor Roth IRA and funded your HSA. It’s been a good year, and now you're sitting there with more extra cash than you know what to do with (nice problem to have).

Tempted to dump it into a plain old taxable brokerage account or buy more gear for your business to get a tax deduction? Let’s hit pause for a second and rethink that. There's one more lever; it’s called the Mega Backdoor Roth.

If your income supports it, you can shove tens of thousands of extra dollars into a Solo 401(k) Roth account every year — growing completely tax-free, forever, with zero required withdrawals (RMDs) in retirement.

It's not for everyone. It's an advanced move; it takes a specific kind of Solo 401(k), and it only matters once you've already filled up the easier buckets.

But if that's you, this is one of the most overlooked moves in the self-employed tax playbook.

How it works

Let’s say you’re 45 years old; you put in the full $24,500 employee contribution into your Solo 401(k). You’re an S-Corp, and your business paid you $100k in W-2 salary, so your biz can contribute $25,000 as the employer contribution (25% of your W-2). That's a total of $49,500.

The Solo 401(k) maximum limit in 2026 for those up to age 49 is $72,000.

$72,000-$49,500 means you have $22,500 of the limit remaining that you can’t use through the normal employee and employer contribution rules. The Mega Back Door Roth method allows you to get that remaining amount into your Solo 401(k) using after-tax compensation, that is, money that has already been taxed, like your S-Corp W-2 salary.

Solo 401(k) Contributions

Employee contributions

| Age | Employee contribution limit — 2026 |

|---|---|

| 49 and under | $24,500 |

| 50–59, and 64+ | $32,500 (inc. $8,000 catch-up) |

| 60–63 (super catch-up) | $35,750 (inc. $11,250 catch-up) |

Your company's employer contribution

| Business type | Employer contribution |

|---|---|

| S-Corp | An additional 25% of the W-2 salary you paid yourself |

| Sole proprietor | An additional 20% of your net earnings from self-employment |

Why would you want to add more to a Solo Roth 401(k)?

The usual move is to invest any additional money you have in a taxable brokerage account. When you sell, you’ll most likely pay 15% capital gains tax on any profits (and potentially the 3.8% NIIT).

With a Roth Solo 401(k) account, if you meet the Roth rules (age 59½ and the funds have been in the account five years+), qualified withdrawals are completely tax-free. Yep, ZERO tax.

The catch? It’s a retirement account, so you can’t get the money whenever you want.

Me? I have a mix of retirement accounts and money in a taxable brokerage account.

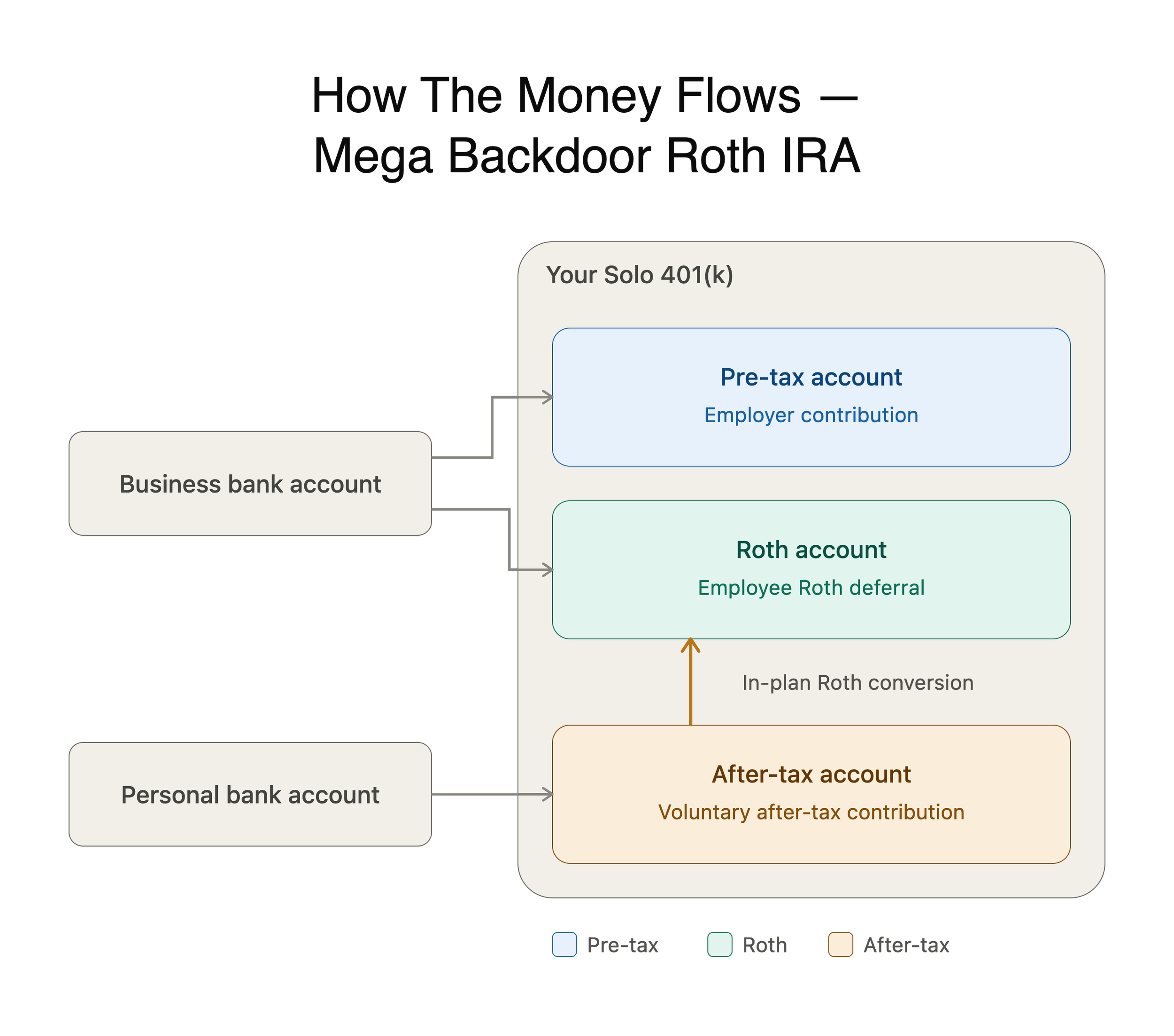

You can also make your regular employee/employer Solo 401(k) contributions to the Solo 401(k) Roth account. This does use up your contribution limits. See the diagram below.

The catch is the Solo 401(k) plan document

Think of the plan document as the rule book for your specific Solo 401(k). Two Solo 401(k)s can have completely different features depending on how the plan was written.

Your free Solo 401(k) plan from Schwab, Fidelity, or E*Trade almost certainly does NOT support this. Those plans are built for the basics — Pre-tax, Roth, employer contribution, often no loan capability — and stop there. To do a Mega Backdoor Roth, your plan document needs two specific features: the ability to make after-tax voluntary contributions, and the ability to either convert them in-plan to a Roth Solo 401(k) or send them out via an in-service distribution to a Roth IRA.

That means a custom plan document from a specialty provider (such as My Solo 401k Financial or Nabers Group, which builds this in) is then usually parked at a broker such as Schwab or Fidelity, which acts as the custodian, with the plan provider as the administrator handling the plan paperwork. The annual fee is a couple of hundred bucks.

Another plus is that these plans qualify you for a $1,500 federal tax credit ($500/year for three years) because the plans include auto-enrollment for employees (that’s only you and your spouse) created by the SECURE Act (2019). So worth it if you're actually going to use the strategy.

How to actually do it

Get a custom Solo 401(k) plan. At the time of writing, Solo 401(k) plans from Schwab, Fidelity, E*Trade, etc do not support the three-sub-account Pre-tax, Roth, and After-tax Mega Backdoor Roth structure. Get a plan from MySolo401k, Nabers Group, Carry, or another provider; they will guide you through the process. If you have an existing Solo 401(k), the new Solo401(k) plan will be created, and then your assets will be transferred. Yes, the paperwork is a pain in the ass, but worth it. Note: You can have only one Solo 401(k) plan with sub-accounts inside it. You can’t have a plan at Schwab and another at Fidelity, for example. Fines and disqualified contributions await if you mess this up.

Max out the normal stuff first. Employee contribution, employer contribution, HSA, Backdoor Roth IRA. The Mega Backdoor is the last lever you pull, not the first.

Do the math on your headroom. For your age group, figure out the maximum Solo 401(k) contribution amount left over after your employee and employer contributions have been made to the Pre-tax and/or Roth accounts. These normal contributions always come from your business bank account, since your employer (that’s you) funds the employees’ Solo 401(k).

Make the after-tax contribution. This should come from your personal bank account into the After-tax sub-account inside your Solo 401(k), not into your regular Pre-tax or Roth bucket. Why your personal account? This way, it makes it clear for record-keeping that the money has already been taxed, unlike the money from your business bank account. Many S-corp owners simply make them from their personal checking account after payroll. This is also a very easy way to keep track of where the after-tax contributions came from.

Convert it — fast. Once the contribution has settled (usually 2-3 days), then convert/move the money from the after-tax account into the Roth account. Do this quickly, because any investment growth on that money before you convert it is taxable when you convert. Check with your brokerage provider (Schwab, Fidelity, etc) on how to make the conversion. It’s usually a phone call or online form.

Invest the funds. Don’t leave the funds in cash; invest them in the usual Three-Fund Portfolio or a Target Date Fund.

Hand the paperwork to your accountant. Tell your plan provider (MySolo401k/Nabers) about the conversion every year. The conversion generates a 1099-R. Make sure whoever does your taxes knows exactly what happened, so it gets reported correctly and doesn't look like a random taxable distribution.

Who is the Mega Backdoor Roth actually for

If you've already filled the Solo 401(k) employee and employer buckets, already done a Backdoor Roth IRA, funded an HSA, and you still have real money left over that you were going to invest anyway. If that's not you yet, go read the post on maxing your 2026 contribution limits first — this is an "advanced level" move, not a starting point.

Talk to your accountant before setting this up. Be aware, though, that some accountants are not familiar with the Mega. Don’t let them tell you the Mega isn’t possible; many don’t encounter it, as most employer plans don’t allow it. Accountants are dealing with an already overly complex tax system and may have missed this hack.

Me

I have a plan from MySolo401k, and my brokerage is Schwab. Over the years, I’ve used the Backdoor Roth strategy to max out my contributions in a few years. Now, as a freelancer at age 53, I take four months off a year as I’ve built a sizable retirement portfolio, so I can now afford to start chilling more.

Plus, I’m Australian (and a U.S. citizen). My people like to retire at 55-60, unlike most Americans who work much longer.

Points to note (don’t screw this up):

After-tax contributions are funds that have been taxed, come out of your personal bank account, and then roll into the Roth account (see the diagram above). They are NOT the same as a direct Roth contribution using your employee and employer contributions. See the diagram above.

Double-check the Solo 401(k) and Mega Backdoor Roth contribution amounts with your accountant.

Keep very good records in a folder on your Mac/PC. The Mega is completely legal, but the IRS can challenge you at any time. Hit them with the records of all the deposits and their sources.

MySolo401k or Nabers is the plan administrator, and brokerages like Schwab and Fidelity are the custodians. They follow the plan created by the plan administrator. The who-is-who is easy to confuse.

The after-tax contribution cutoff date to get the money into the account is your tax filing date.

Don’t forget to file IRS Form 5500-EZ annually if your Solo 401(k) combined balance exceeds $250k. The fine for failing to file could be up to $150,000.

Even if you don’t have spare cash this year, consider setting up a custom Solo 401(k) plan so it’s in place and ready to go.

What’s the end goal?

As freelancers, self-employed, or solopreneurs, we want to build up a large enough investment nest egg that can start generating income in later years. That income means you can slow the hustle or just peace out entirely. Read the post here about how much you’ll need.

We will get rich, slow. The Mega Backdoor Roth is just for the years you're doing better than slow.

Send this article to your people; freelancers need to support each other.